The corporate matrix is simple. Investors invest in the business. If the business succeeds, the investors get all the benefits — in either dividends or capital gains.

The spolu matrix is also simple. If the spolu is successful, it puts a significant portion of that profit back to the stakeholders: investors, employees, customers, suppliers, philanthropy, and re-investment obligations.

Which matrix works better for you?

To help you answer this question, let’s create another hypothetical business. Here are the basic statistics of B-Z Manufacturing:

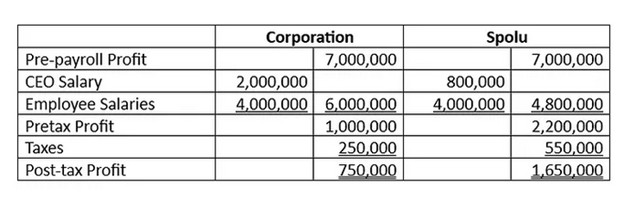

· 100 employees, who earn $40,000 a year. Total annual payroll is $4,000,000

· 1 CEO. The corporate CEO makes $2,000,000 a year. The spolu network’s 20x multiplier means its CEO makes $800,000.

· The pre-payroll profit is $7,000,000.

· Corporate taxes are 25%.

· All spolu employees are fully vested to share the profit distribution.

The corporate model would move $750,000 to the investors.

The spolu model will move $1,650,000 to stakeholders. One-sixth goes to the investors, which means $275,000. Another sixth goes to the employees, so $275,000 is split between the CEO and the employees. The CEO gets a bonus of $45,833. Each employee gets a bonus of $2,291. This is a 5.7% “profit sharing” bonus.

Of course, the investors and corporate CEOs would prefer the corporate model. This system works better for them.

But notice the spolu employees get a bit of those profits. The corporate employees do not. Which company is going to be more motivated to perform better next year?

This example does not show two other motivational advantages. First, the spolu will also be getting other spolu income, whereas the corporation does not. Second, the spolu will have a more loyal customer base.

The first question I would ask is: “If the spolu and corporations are direct competitors, which one is more likely to steal market share from the other?”

The second question is: “Which — the corporation or the spolu — would be a better long term investment?”

Published on Medium 2024

Spolu 17: Management Salaries, Part 2